by Kayla Young, WFAE and La Noticia

This story was originally published by WFAE and La Noticia on April 17, 2023 as part of WFAE’s Race & Equity Project, EQUALibrium.

Earlier this year, Yesenia Rios moved into her first home, a three-bedroom house in Kannapolis.

The atmosphere on moving day felt a bit like a block party. Parked cars lined the street and dozens of people, from elected officials to church leaders, gathered in her front yard to celebrate.

This day came after years of work, marked by ups and downs.

“Five years ago, I moved from New York looking for a new start for me and my children. I’ve been moving for the last five years from place to place. This will be my fifth time moving, and this will be the last,” she told the crowd.

Rios is one of three heads of household to become a homeowner this year through Habitat for Humanity in Cabarrus County, north of Charlotte. To qualify, she put in about 250 work hours and helped build the house with other Habitat volunteers.

She explained in a phone interview that Habitat was her pathway to achieving stability and affordable homeownership.

“When I moved to this state, things got complicated for me. I ended up in a Christian shelter,” she said.

She met Habitat volunteers at the shelter, which had a housing program, and began her journey to becoming a homeowner.

Visitors wait to congratulate Yesenia Rios, center, on receiving the keys to her first home. Photo: Kayla Young, WFAE/La Noticia

Young, rapidly growing demographic

Rios, who was born in the United States and grew up in Mexico, made homeownership a priority. And in many ways, she represents the future of the home-buying market.

Over the next 20 years, Latinos are forecast to represent the bulk of new homebuyers in the U.S., despite persisting economic and structural barriers. That’s what researcher Jun Zhu and her colleagues at the Urban Institute in Washington, D.C., found.

“Between 2020 and 2040, if you’re talking about the homeownership increase, 70% of the new net homeowners are actually Hispanic,” Zhu said. “This is a big deal.”

Latinos are the fastest-growing demographic in North Carolina and the U.S. and they’re a younger demographic, which means more of them are entering their peak years for home buying.

“They are younger. They have less income and wealth. And if we do the comparison for the credit score, they have a little bit lower credit score,” Zhu said. “But family size. [They have] large family sizes, and the majority of them actually live in a multigeneration family. So that’s very unique to Hispanics.”

Mercedes Dockery has worked as a real estate agent in the Charlotte area for the past seven years. She says around 90% of her clients are Latino.

“They are looking for land. They love to have land and to be spaced out from other houses,” she said.

That can mean leaving Charlotte, where the affordable housing market is limited. Many of Dockery’s clients are looking at places like Monroe, Gastonia or Fort Mill.

UNC Charlotte found that only 3.8% of the homes sold in Charlotte last year were valued under $150,000. (That’s a little under the value of Rios’ new home in Kannapolis). About 25% were valued under $300,000.

Securing a mortgage for under $150,000 can be difficult, said Tara Roche of Pew Trust’s home financing project. She says the lack of access to lower-value mortgages is an issue leading certain homebuyers to explore alternative financing, like land contracts or rent-to-own agreements.

“Black, Hispanic and Indigenous families, and some households in rural geographies, have lower levels of mortgage lending and higher levels of alternative financing,” Roche said.

“Alternative financing arrangements can come with greater risks and higher costs for people who are on their pathway to homeownership.”

The demographic most likely to use alternative financing was Latino buyers. Pew Trusts found that 34% of Latino homebuyers had used alternative financing, compared to 23% of Black homebuyers and 19% of white homebuyers.

“For people who are using land contracts, for example, they don’t get the deed upfront, so that means they can’t tap into any of the equity that would be built in the home the way you could if you were a mortgage holder,” Roche said. “You’re at increased risk of foreclosure or eviction because you don’t hold (the) title to that home.”

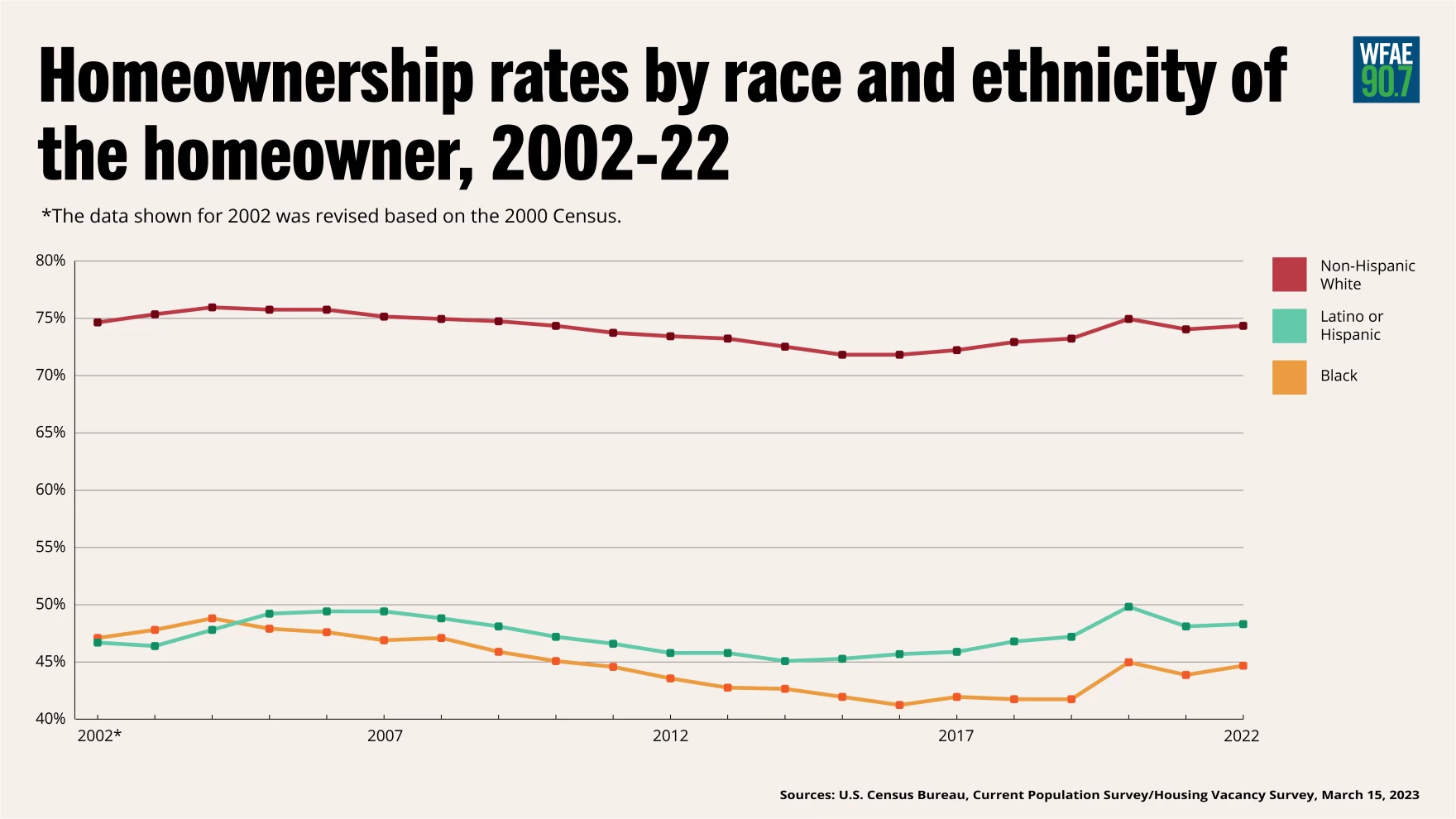

Graphic: Layna Hong, WFAE

Urban Institute researcher Todd Hill explains that structural barriers continue to depress homeownership rates in communities of color.

“Much like what we’ve seen with Black homeownership initiatives and marginalized communities and communities of color that attempt to pursue homeownership, you still have a number of systemic and historical policies that have been in place that have impacted the ability for these particular communities to access credit and pursue homeownership.

“You still have a trust deficit that exists with the Hispanic community, with (the) African American community and other communities that have traditionally been sort of locked out of homeownership opportunities,” Hill said.

Analysis by Construction Coverage identified a 26% gap in the homeownership rate between whites and people of color who are homeowners in the Charlotte metro area. That’s a few percentage points higher than the nationwide gap of 22.3%. Even with the forecast growth in Latino home buying, this gap isn’t expected to narrow by much in the coming decades.

To encourage sustainable homeownership, Hill says there’s a need to educate prospective buyers about their financing options. He says there are more than 2,500 down-payment assistance programs nationwide.

“I think really one of the factors is housing counseling. When you look at, for example, the ability for a counselor to navigate the mortgage process, they can help to build knowledge and confidence in the home buying process,” he said. “A counselor can also assist in case of language barriers.”

Roche said she would also like to see alternative financing recognized on a policy level, to protect buyers from losing their investments.

Listen to the original story at WFAE here.

This story is part of ‘I Can’t Afford to Live Here,’ a collaborative reporting project focused on solutions to the affordable housing crisis in Charlotte.

WFAE and La Noticia are part of the Charlotte Journalism Collaborative (CJC), launched by the Solutions Journalism Network with funding from the Knight Foundation. The CJC strengthens the local news ecosystem and increases opportunities for engagement. It is supported by a combination of local and national grants and sponsorships. For more information, visit charlottejournalism.org.